On Feb 26, 2026, Theo introduced a USD-denominated “stablecoin”, “backed” by a delta-neutral gold strategy. The strategy holds spot gold and achieves a delta-neutral – i.e. stable with respect to the USD – position by selling futures.

On surface, the stats look great;

- Higher open interest than BTC/ETH, implying more liquid markets

- Less volatility, implying a less risky strategy than, e.g. tokenised BTC hedge funds

- Higher intrinsic yield than a similar BTC/ETH strategy

The “stablecoin”, thUSD, generates yield two ways: a) lend the spot gold to retailers, and b) exploit the futures-spot delta.

The yield, backtested over 2025, is composed of 2.5% from lending and ~6.7% from the futures-spot trade, also known as roll yield. Over the past year, USDC lending in Aave – which is overcollateralised – generated ~3.7%, outperforming Theo’s proprietary blackbox lending strategy by ~50%. As for the roll yield, I’ll quote Bloomberg’s Nov 11, 2025 article:

Over the past 5 years, the gold forward curve has steepened into deeper contango as a result of the higher interest rate regime – the purple line (2025) is more upward sloping compared to the orange line (2020)

Coincidence or malice, basing the estimated yields on one of the highest roll yield years in recent history gives an inflated image of the long-term yield of the asset.

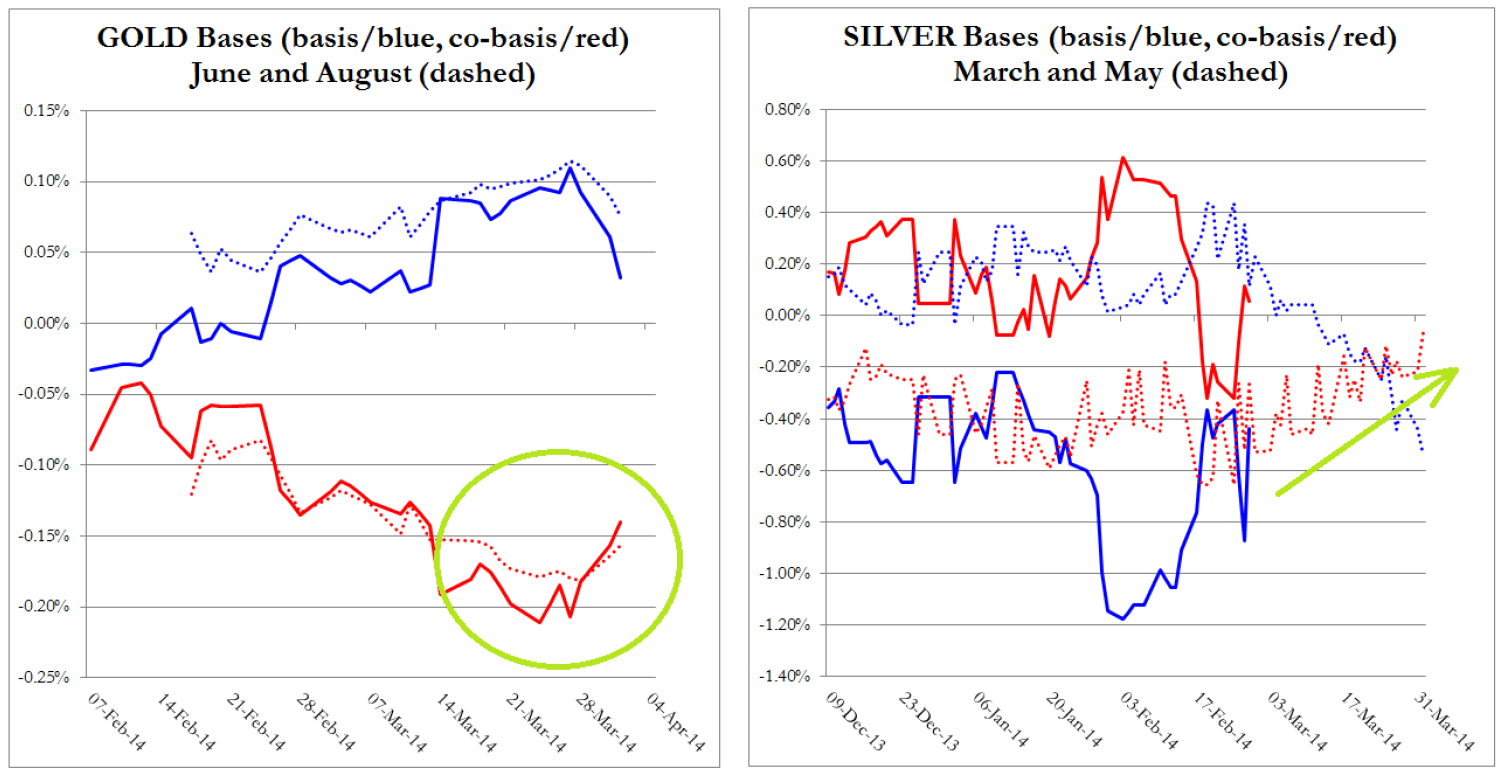

The issuer claims that the strategy “generates yield regardless of whether gold goes up or down”. This might be true when the market is in contango, i.e. futures trade at higher prices than the spot equivalent. The opposite is called backwardation and, unlike the issuer indicates, has happened – even with gold. See the below chart from GoldBroker.com, which shows extensive backwardation (blue line below 0) in February of 2014.

GoldBroker.com goes as far as positing

There will come a time when there will be no gold or silver available to trade against paper currencies. This will be preceded by a large increase in backwardation, all the way to permanent backwardation.

If this were to happen, assuming the spot gold lending profits do not exceed the basis backwardation, the strategy would turn negative. Permanently.

As usual with these types of tokenised strategy “stablecoins”, the story told to the average retail holder of the stablecoin is polished, arguably all the way to a lie. See the following excerpt from the announcement article:

For Depositors: thUSD enables easy access to industry-leading yields as a dollar-denominated savings instrument backed by the world’s oldest store of value.

Catch the lie?

In addition to being nowhere near industry-leading USD yield, because thUSD is “backed” by the combination of a long and a short position, it is not backed by gold, “the world’s oldest store of value”. Its value is derived from the performance of that strategy. Its value is not derived from having explicit claim on any asset.

This flies in the face of the primary assertion and title of the article: “Introducing thUSD: The Gold Standard is Back” – the gold standard is not back. The gold standard was based on the fact that one unit of money would be interchangeable with a given quantity of gold. The gold standard is not back – you cannot exchange thUSD for a given quantity of gold. You are still accounting in USD. You are not backstopped by gold.

It’s a good story, but it is a bold-faced lie.

I’m not saying the product wouldn’t be good. I’m not saying there’s no place for a tokenised strategy like this. USDai, USDe, and many others have been successful and have a place in the market. But none of them are stablecoins.